How Saudis Access Cryptocurrency Exchanges: Methods, Risks & Regulations

Crypto Access Cost Calculator

Compare Your Options

Notes:

These estimates are based on current Saudi market conditions. Actual costs may vary based on platform and market conditions.

Regulatory risk is not reflected in these calculations and could lead to account freezes or other restrictions.

When it comes to cryptocurrency access in Saudi Arabia the ways Saudis reach global platforms despite local restrictions, the landscape feels like a maze. The Kingdom officially calls virtual currencies “illegal and unlicensed,” yet more than 11% of the population holds crypto assets. How do they get around the rules? Below you’ll find the most common routes, the pitfalls to watch, and what the regulators are likely to change next.

Key Takeaways

- Saudis mainly use three channels: international exchanges, peer‑to‑peer (P2P) platforms, and crypto ATMs.

- Bank integration is prohibited, so users rely on VPNs, gift‑card swaps, and cross‑border payment processors.

- Binance, Bybit and OKX dominate the exchange traffic, handling roughly $850million of daily Saudi volume.

- Regulatory risk remains high: SAMA can freeze accounts and the Anti‑Money Laundering Law may be applied retroactively.

- Upcoming drafts from SAMA and the Capital Market Authority could reshape the market by late2025.

Regulatory Landscape - What’s Actually Allowed?

The Saudi Central Bank (SAMA Saudi Arabia’s monetary authority) has repeatedly warned that banks may not handle crypto unless they receive explicit approval. However, no specific law bans individuals from owning or trading virtual assets, so the sector lives in a gray zone.

Two legal references matter most:

- Article18 of the Anti‑Money Laundering Law Royal Decree M/20, 2017 defines “funds” broadly enough to include digital tokens.

- The Saudi General Authority of Zakat and Tax tax body states that personal crypto gains are not subject to capital‑gains tax, though corporate holdings face a 15% rate.

Because the law is ambiguous, many users treat crypto like any other foreign‑exchange activity-just outside the formal banking system.

Primary Access Channels

Three methods account for almost all Saudi crypto activity. Below is a quick snapshot, followed by a deeper dive.

| Method | Typical Platforms | Typical Fees | Regulatory Risk |

|---|---|---|---|

| International Exchange | Binance, Bybit, OKX | ~3.7% total (deposit + withdrawal) | Account freeze if SAMA queries |

| P2P Marketplace | LocalBitcoins, Paxful | 2-5% depending on payment method | Fraud risk, limited legal recourse |

| Crypto ATM | Various local ATMs (Riyadh, Jeddah, Dammam) | ~4.2% per transaction | Cash‑out limits, no banking link |

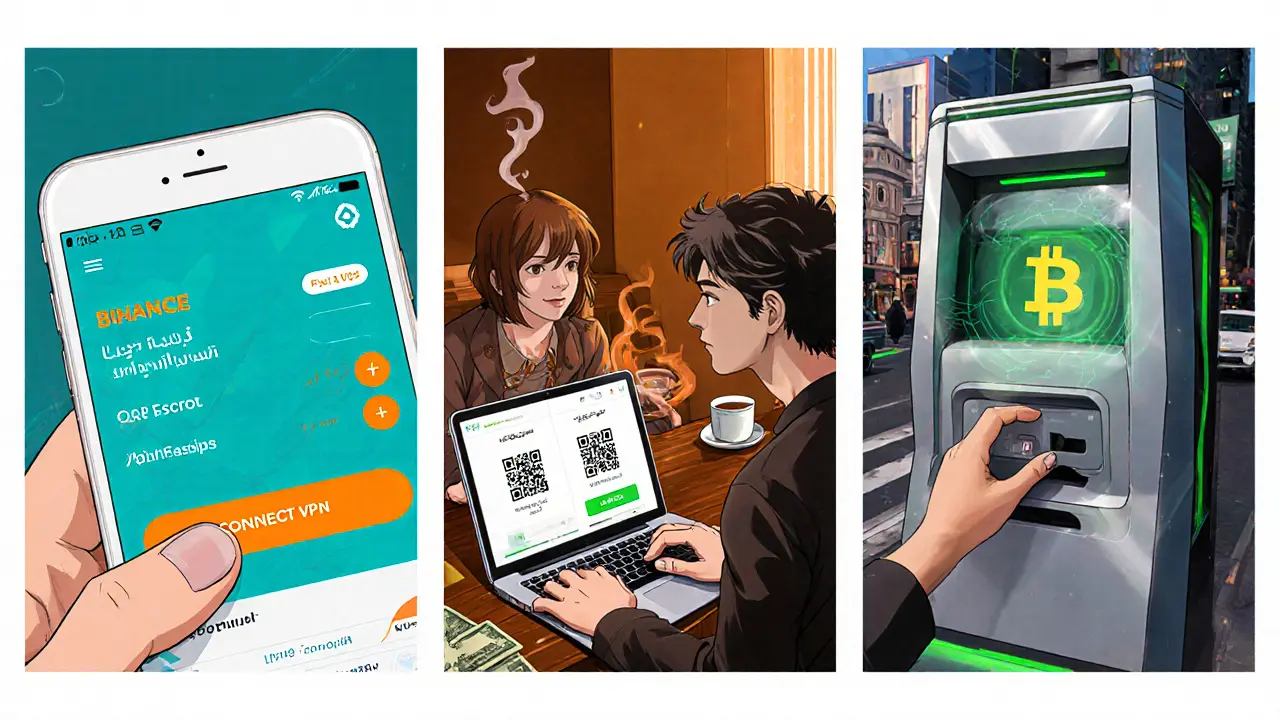

1. International Exchanges - The Heavy Hitters

International platforms dominate because they provide deep liquidity, advanced trading tools, and English‑language support. The three biggest for Saudis are:

- Binance global crypto exchange with a large Saudi user base

- Bybit derivatives‑focused exchange popular among day traders

- OKX exchange known for low fees and DeFi products

Getting on one of these usually follows a 4‑step flow:

- Download the mobile app or visit the website (many users first connect via a VPN to avoid throttling).

- Create an account and enable multi‑factor authentication.

- Complete KYC using a Saudi national ID and a passport‑style selfie. About 68% of Saudis succeed on the first try.

- Fund the account through a workaround-most commonly a P2P‑to‑exchange bridge, a crypto‑friendly payment processor, or a gift‑card conversion.

Once funded, users can trade, stake, or transfer assets. The biggest pain point is withdrawal: without a Saudi bank link, many rely on crypto‑to‑fiat services like NOWPayments or transfer USDT to a friend who cashes out abroad.

2. Peer‑to‑Peer (P2P) - The Grassroots Solution

P2P platforms let buyers and sellers meet directly, often using a local bank transfer on the seller’s side. Two platforms dominate:

- LocalBitcoins P2P marketplace with escrow protection

- Paxful global P2P network supporting many payment methods

A typical SAR‑to‑USDT trade goes like this:

- Post a buy order specifying SAR as the payment currency and USDT as the receipt.

- Choose a seller who accepts a local bank (Alinma, AlRajhi are most common).

- Transfer SAR to the seller’s account, then confirm receipt on the platform.

- The escrow releases USDT to your exchange wallet.

This method accounts for roughly 37% of all Saudi fiat‑to‑crypto conversions. It’s cheap-average fee 2.5%-but users must vet counterparties carefully; fraud cases totalled SAR1.2billion in 2024.

3. Crypto ATMs - Cash‑First Access

There are 127 crypto ATMs spread across Riyadh, Jeddah, and Dammam. They work like a regular ATM but dispense Bitcoin or USDT instead of cash. Steps are simple:

- Scan a QR code from your mobile wallet.

- Select the amount of crypto you want.

- Insert SAR cash (maximum SAR10,000 per transaction).

- Receive the crypto in your wallet instantly.

ATMs charge about 4.2% and have daily limits, but they’re useful for users who dislike online banking entirely.

Workarounds for the Banking Ban

Since Saudi banks cannot directly handle crypto, users get creative:

- VPNs - 28% of Saudis subscribe to services like NordVPN solely to reach exchange sites without throttling.

- Gift‑card swaps - Platforms such as PayPal or local e‑gift services let you buy a $100 Amazon card, then convert it to crypto on an exchange.

- Cross‑border processors - Wise and Revolut let you fund a foreign bank account that the exchange accepts.

All of these add a small fee but keep the money flow outside the Saudi banking system, which reduces the chance of a freeze.

Risks You Can’t Ignore

Even if you master the technical steps, regulatory and operational risks linger:

- Account freezes - SAMA has requested information from exchanges. Binance froze a SAR150,000 account for 87 days after a compliance check in early2025.

- Fraud - P2P scams still cause losses; the Cybercrime Investigation Department logged 1,842 cases in 2024.

- Liquidity crunches - Global market swings can make it hard to convert crypto back to SAR quickly, especially on smaller exchanges.

The safest approach is to keep only a modest amount on an exchange, move the rest to a hardware wallet, and use P2P only for the occasional cash‑in.

What’s Coming Next? Regulatory Outlook

Both SAMA and the Capital Market Authority (CMA) have promised drafts by Q42025. Expected changes include:

- Clear licensing pathway for a domestic crypto‑exchange hub.

- Limited “whitelisted” tokens for institutional investors.

- Mandatory AML reporting for all crypto transactions above SAR50,000.

If those rules pass, we may see the first Saudi‑registered exchange within two years, which could dramatically cut the need for VPNs and foreign payment processors.

Practical Step‑by‑Step Guide for New Users

Here’s a concise checklist that covers the whole journey from zero to a funded exchange account.

- Secure a reliable VPN service (NordVPN, ExpressVPN) and test connectivity to Binance/Bybit.

- Create a new email address dedicated to crypto.

- Download the exchange app of your choice and start the registration.

- Enable 2FA via Google Authenticator.

- Prepare a scanned copy of your Saudi national ID and a selfie for KYC.

- Complete KYC; if rejected, try a different exchange or use a local ID verification service like CertiK Arabia (sandbox‑approved).

- Choose a funding method:

- First‑time users often start with a P2P purchase of USDT using a local bank transfer.

- Alternatively, buy a $50 Amazon gift card, convert it on a micro‑exchange, then send USDT to your main wallet.

- Deposit the USDT into your exchange wallet; verify the deposit on the blockchain explorer.

- Start trading, but keep initial position under 10% of your total crypto holdings.

- When you need cash, move crypto to a P2P buyer or use a crypto ATM for a quick SAR withdrawal.

Most users report that mastering these steps takes 2-3weeks, but the community on the Telegram group "Saudi Crypto Traders" can answer questions within minutes.

Bottom Line

Even though the legal environment stays murky, Saudi residents have built a robust, community‑driven ecosystem to access global exchanges. Whether you prefer the slick interface of Binance, the personal touch of LocalBitcoins, or the immediacy of a crypto ATM, each path carries its own cost and risk profile. Stay savvy, keep a small portion on any exchange, and watch for the upcoming regulatory drafts that could make the whole process a lot cleaner.

Frequently Asked Questions

Can I use a Saudi bank card to buy crypto on Binance?

Directly linking a Saudi bank card is not allowed. Most users first buy USDT on a P2P platform using a local bank transfer, then deposit that USDT into Binance.

Is it legal to own Bitcoin in Saudi Arabia?

The law does not criminalize ownership, but any transaction can be scrutinized under the Anti‑Money Laundering Law. A 2023 fatwa declared Bitcoin permissible under Sharia, which many users reference.

Do I need a VPN to access crypto exchanges?

A VPN isn’t mandatory, but it helps avoid occasional throttling and keeps your IP out of SAMA monitoring tools. Around 28% of Saudi traders subscribe to a VPN for this reason.

What fees should I expect when using a crypto ATM?

Most ATMs charge between 3.5% and 4.5% per transaction, plus a small flat fee for small amounts. Check the kiosk screen before confirming.

Will upcoming regulations make crypto harder to access?

Drafts suggest a licensing regime that could legitimize local exchanges, which would actually simplify access. However, stricter AML reporting may increase compliance costs for users.

Comments

Matthew Homewood

May 20, 2025 AT 11:25Saudi crypto users navigate a fragmented ecosystem that combines offshore exchanges, P2P marketplaces and a handful of ATMs. The lack of a domestic licensing framework forces traders to rely on VPNs to mask their IP addresses when accessing Binance, Bybit or OKX. KYC procedures typically require a national ID and a selfie, and about two‑thirds of applicants succeed on the first attempt. Funding the accounts is the real bottleneck, because Saudi banks cannot directly accept fiat for crypto purchases. Most traders bridge the gap by buying USDT on a P2P platform with a local bank transfer and then moving the tokens to an exchange wallet. Gift‑card swaps are another creative workaround, turning an Amazon voucher into crypto on micro‑exchanges. Cross‑border payment processors such as Wise or Revolut act as intermediaries, allowing a foreign bank account to receive SAR and forward it to the exchange. The fee structure varies: international exchanges charge roughly 3.7 % total, while P2P trades sit around 2‑5 % and crypto ATMs hover near 4.2 %. Regulatory risk remains high; SAMA has frozen accounts in the past when compliance checks flagged suspicious activity. Users mitigate this by keeping only a small balance on the exchange and storing the bulk in hardware wallets. Fraud is still a concern on P2P platforms, with reported losses exceeding a billion Saudi riyals in 2024. Liquidity crunches can occur during market stress, making rapid fiat conversion difficult. The community has built support channels on Telegram and Discord, where newcomers can get step‑by‑step guidance. Despite the obstacles, the ecosystem demonstrates resilience, adapting quickly to regulatory signals. Looking ahead, drafts for a licensed Saudi exchange could streamline access, reduce reliance on VPNs, and introduce clearer AML reporting requirements.

Shane Lunan

May 28, 2025 AT 21:32VPNs are the cheapest way to dodge SAMA throttling.

Jeff Moric

June 6, 2025 AT 07:38It's impressive how the community has built a safety net around the gray‑zone regulations. By sharing step‑by‑step guides, experienced traders lower the entry barrier for newcomers. Keeping only a modest amount on exchanges and moving the rest to hardware wallets is a solid risk‑mitigation strategy. Diversifying funding sources-using both P2P and crypto ATMs-helps spread the regulatory exposure. Remember that staying informed about upcoming SAMA drafts can save you from unexpected freezes.

Bruce Safford

June 14, 2025 AT 17:44What they don't tell you is that SAMA has a hidden backdoor to monitor every VPN tunnel. The leaks suggest that even encrypted traffic gets tagged and flagged for review. If you think using a gift‑card swap is safe, think again; those services log your purchase data and could hand it over. Many traders have reported accounts frozen overnight after a single suspicious transfer. The truth is the whole system is designed to funnel crypto activity into state‑controlled channels.

Blue Delight Consultant

June 23, 2025 AT 03:51The philosophical underpinning of crypto adoption in Saudi Arabia reflects a tension between decentralized ideals and centralized control. While the religious fatwa deems Bitcoin permissible, the monetary authority remains wary of uncontrolled capital flows. This dichotomy creates a unique environment where users must navigate both legal ambiguity and technical hurdles. It is essential to weigh the ethical implications of bypassing banking regulations against the desire for financial sovereignty. Ultimately, the evolution of policy will dictate whether this tension resolves or deepens.

Wayne Sternberger

July 1, 2025 AT 13:57Indeed, the community's mentorship role cannot be overstated. By offering clear, step‑by‑step instructions, we empower newcomers to avoid costly missteps. Keeping a small balance on the exchange while storing the majority in a hardware wallet remains best practice. Diversifying payment methods-P2P, gift cards, and ATMs-further reduces exposure. Continuous education will be key as regulatory drafts emerge.

Gautam Negi

July 10, 2025 AT 00:03While many celebrate the burgeoning crypto scene, I remain skeptical of its sustainability under current Saudi policies. The reliance on VPNs and offshore entities could crumble if enforcement intensifies. Moreover, the promised domestic exchange hub may never materialize, leaving users stranded in a legal limbo. One must consider the hidden costs of constant workarounds and the psychological toll of operating in secrecy. In the end, the glitter of decentralization may veil a fragile foundation.

Shauna Maher

July 18, 2025 AT 10:10Don't be naive, Gautam. The state already has the tools to shut down every workaround you cherish. Every VPN server is a target, and every gift‑card platform is under scrutiny. The moment SAMA enforces the new AML thresholds, the entire ecosystem will grind to a halt. Accept that your optimism is a luxury you can't afford.

Kyla MacLaren

July 26, 2025 AT 20:16The community really shines when users share their own hacks for funding exchanges. Simple tips like using a friend’s overseas account can make the process smoother. Keeping communication channels open ensures we all stay ahead of regulatory changes. It's great to see newcomers feeling supported.

Linda Campbell

August 4, 2025 AT 06:22While collegial assistance is commendable, it is imperative to acknowledge the inherent risks associated with such circumvention. The transfer of assets through foreign intermediaries may contravene anti‑money‑laundering statutes, exposing participants to legal repercussions. Consequently, a measured approach, favoring compliance over convenience, should be advocated. Continuous monitoring of regulatory developments is essential to mitigate exposure.

John Beaver

August 12, 2025 AT 16:29For anyone looking to start, the fastest route is to purchase USDT on a reputable P2P platform using a local bank transfer, then move the tokens to a major exchange. This method bypasses the need for direct fiat deposits and keeps transaction fees relatively low.

EDMOND FAILL

August 21, 2025 AT 02:35The P2P approach indeed streamlines onboarding, especially when combined with a reliable escrow service. Ensuring both parties have verified profiles reduces fraud risk dramatically. Additionally, using a hardware wallet for long‑term storage adds a vital layer of security.

Jennifer Bursey

August 29, 2025 AT 12:41From a fintech integration perspective, the current Saudi crypto workflow embodies a hybrid on‑ramp/off‑ramp architecture fraught with compliance latency. Leveraging modular API layers for KYC verification can accelerate onboarding while maintaining regulatory fidelity. Moreover, dynamic fee arbitration algorithms could optimize cost structures across exchange, P2P, and ATM channels. Stakeholders should prioritize interoperable standards to future‑proof the ecosystem against impending legislative shifts.

Maureen Ruiz-Sundstrom

September 6, 2025 AT 22:47Your so‑called “modular API layers” are nothing but buzzword fluff that distracts from the real issue: users are forced into a clandestine maze of workarounds. Instead of preaching interoperability, you should acknowledge that the current system is fundamentally broken and prioritize genuine regulatory clarity.

Kevin Duffy

September 15, 2025 AT 08:54Love seeing the community pull together! 🙌 Keep sharing those hacks and stay safe out there. 🚀📈

Tayla Williams

September 23, 2025 AT 19:00While the optimism is admirable, it is essential to temper enthusiasm with a sober assessment of systemic vulnerabilities. The reliance on informal networks may inadvertently perpetuate exposure to illicit activities, thereby undermining the integrity of the emerging market.

Brian Elliot

October 2, 2025 AT 05:06The upcoming licensing drafts could indeed streamline access, but they also risk imposing stricter AML reporting that may deter casual participants. Balancing regulatory oversight with user convenience will be a delicate act for policymakers.

Marques Validus

October 10, 2025 AT 15:13Oh boy, here we go again-another policy rollercoaster! 🎢 The drama of waiting for those drafts feels like watching a crypto bubble inflate in slow motion. Meanwhile, traders are juggling VPNs, gift‑cards, and ATMs like circus performers. If the regulators finally drop a legit exchange, we might actually get to chill and trade without a detective on our tail. Until then, buckle up, because the crypto carnival isn’t over yet.

Mitch Graci

October 19, 2025 AT 01:19Wow, what a revolutionary insight-crypto ATMs exist! 🙄 Surely this will completely change the game and make all the regulatory hurdles vanish overnight!!!

Jazmin Duthie

October 27, 2025 AT 10:25And just like that, the ATM will solve everything. 🙃